Real estate tech is one of the fastest-growing startup verticals in 2026. Proptech companies raised over $19 billion globally last year, and that number keeps climbing. But the financial side of these businesses is uniquely complex. Revenue models blend SaaS subscriptions with transaction-based fees. Assets straddle both digital and physical worlds. Tax obligations shift depending on how deeply a platform touches actual property transactions.

If you're founding, funding, or advising a proptech startup, your accounting can't follow a generic playbook. You need a framework built for this specific vertical. That's exactly what this guide delivers: a practical accounting resource designed for real estate technology startups at every stage. Whether you're pre-revenue or scaling past Series A, the principles here will keep your books clean, your taxes filed correctly, and your investors confident.

We built this guide from real experience working with proptech founders. Every section addresses a specific pain point. Let's get into it.

Accounting for real estate tech startups means tracking revenue, expenses, and tax obligations across a business model that often combines software delivery with property-related transactions. It matters because misclassified revenue or poorly structured books can kill a funding round overnight.

Here are the three most important things to know:

The bottom line: proptech accounting requires vertical-specific knowledge. Generic startup bookkeeping won't cut it.

From an accounting firm's perspective, real estate tech clients present a blend of challenges you won't see in a typical SaaS company. The first major difference is hybrid revenue streams. Your clients in this space rarely earn money from just one source. A property management platform might charge monthly subscriptions, take a percentage of rent collected, and earn referral fees from service providers. Each stream has different recognition rules under ASC 606, and lumping them together creates audit risk.

The second nuance involves the treatment of real estate data. Many proptech startups license or aggregate property data as a core part of their product. The costs of acquiring, cleaning, and maintaining that data don't fit neatly into standard expense categories. Some qualify as intangible assets. Others are operating expenses. The classification affects both your P&L and your balance sheet.

Third, proptech startups often operate in regulated environments. If a platform handles escrow funds, earnest money, or security deposits, trust accounting rules apply. These aren't optional. A single compliance failure can result in license revocation or legal action. Your chart of accounts, internal controls, and reconciliation processes all need to reflect this regulatory reality from day one.

Your chart of accounts is the skeleton of your financial reporting. For proptech startups, it needs more granularity than a standard tech company setup. You'll want separate revenue accounts for each distinct income stream: subscription fees, transaction commissions, data licensing, and referral income. Expense accounts should distinguish between general R&D and capitalized software development costs, since the tax and reporting treatment differs significantly. If your platform holds any client funds, you need dedicated trust liability accounts that stay completely isolated from operating accounts. Naming conventions matter too. Use descriptive names that make sense to both your internal team and external auditors. "Revenue - Platform Transaction Fees" is far more useful than "Revenue - Other." Clear naming prevents misclassification, which is the single most common bookkeeping error we see in this vertical.

Here are five example accounts commonly added for proptech companies:

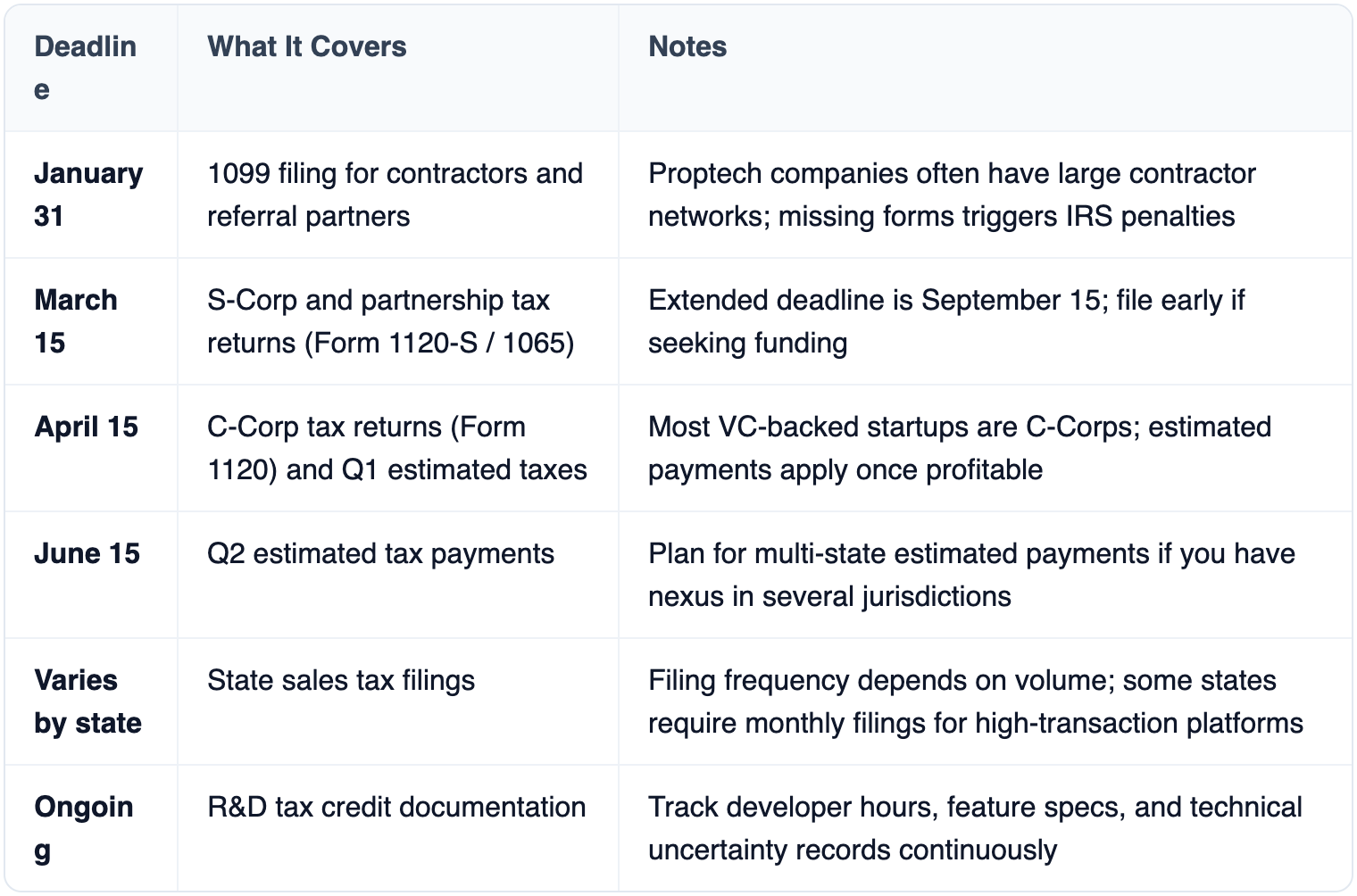

Real estate tech startups face a tax environment shaped by both their software business model and their proximity to property transactions. Multi-state operations can create filing obligations in states where you've never set foot. R&D tax credits offer meaningful savings, but only if you document qualifying activities correctly throughout the year.

Choosing the right accounting software is essential for proptech startups. Here's what your platform needs to handle:

Do I need a specialized accountant for my proptech startup, or can any CPA handle it?

A general CPA can manage basic bookkeeping. But proptech-specific issues like trust accounting, ASC 606 multi-stream revenue recognition, and multi-state nexus analysis require specialized knowledge. Look for firms with direct experience serving real estate technology companies. The wrong guidance on revenue recognition alone can cost you a funding round.

How should a seed-stage proptech startup set up its books?

Start with a clean chart of accounts that separates your revenue streams from day one. Even if you only have one income source now, build the structure for growth. Use accrual-basis accounting, not cash-basis. Investors and auditors expect it. Set up your trust accounts immediately if you handle any client funds, even small amounts.

Can proptech startups claim R&D tax credits?

Yes, and most should. Building proprietary algorithms, developing new platform features, and creating data processing tools all qualify as research activities under IRC Section 41. The key is documentation. Track developer hours by project, save technical specs, and record the specific uncertainties your engineering team worked to resolve.

How do I handle revenue from marketplace transactions versus subscriptions?

These are separate performance obligations under ASC 606. Subscription revenue is recognized ratably over the contract term. Marketplace transaction revenue is typically recognized at the point of transaction completion. Mixing them into one revenue line creates problems during audits and due diligence.

When should I hire a fractional CFO versus a full-time controller?

Most proptech startups benefit from a fractional CFO between seed and Series A. You need strategic financial guidance for fundraising, pricing models, and burn rate management. A full-time controller makes sense once your monthly transaction volume and team size demand daily financial oversight, usually around the Series B stage.

Getting your accounting right from the start saves you from expensive cleanups later. The real estate tech vertical demands more precision than most startup categories. Your revenue is more complex, your regulatory exposure is broader, and your investors expect cleaner financials because of the asset class you touch.

Start with a properly structured chart of accounts. Implement trust accounting controls if you handle any third-party funds. Document your R&D activities every sprint, not just at tax time. And find an accounting partner who actually understands proptech, not one who'll learn on your dime.

This guide to accounting for real estate tech startups gives you the framework. The execution is up to you. Build the financial infrastructure now that your Series A investors will expect to see later. Your future self will thank you for it.