PropTech is reshaping how we buy, sell, manage, and invest in real estate. But behind every smart building platform and AI-driven property tool sits a messy accounting reality. Revenue recognition gets tricky. Capitalization rules blur. Tax obligations shift depending on your business model. If you're running a PropTech startup or advising one, getting the financial foundation right isn't optional. It's survival. This guide to accounting for PropTech startups breaks down the specific challenges, structures, and strategies you need to know. Whether you're pre-seed or scaling past Series A, the financial playbook matters more than most founders realize. Treat it like your product roadmap: ignore it, and you'll build on a foundation that cracks.

PropTech accounting is the financial management of startups that build technology products for the real estate industry. It matters because PropTech companies often straddle two worlds: software and real estate. That creates unique revenue, cost, and compliance considerations that generic startup accounting doesn't address.

Here are the three most important things to know:

The bottom line: PropTech accounting requires a hybrid approach. You need someone who understands both software economics and real estate financial mechanics.

From an accounting firm's perspective, PropTech clients don't fit neatly into existing industry templates. Your clients in this space are building software, but their revenue often depends on real estate transaction cycles. Those cycles are longer, more seasonal, and more regulated than typical SaaS sales cycles.

The first major nuance is revenue bundling. Most PropTech platforms package multiple deliverables into a single contract: a software license, implementation services, data feeds, and sometimes transaction-based fees. Under ASC 606, each performance obligation must be identified and priced separately. This isn't theoretical. Auditors will push back if you lump everything together.

The second nuance involves trust accounting. If your client's platform touches tenant payments, security deposits, or escrow funds, those dollars must be segregated in trust accounts. Commingling client funds with operating cash is a compliance violation in most states. This creates a parallel set of books that many SaaS-focused accountants haven't managed before.

A third distinction is the cost structure. PropTech startups often carry real estate data licensing fees, MLS integration costs, and property database subscriptions. These recurring costs don't map to standard SaaS cost-of-revenue categories and need thoughtful classification.

A standard SaaS chart of accounts won't capture the full picture for a PropTech company. You'll need accounts that reflect real estate-specific revenue streams, trust fund liabilities, and data acquisition costs. Naming conventions should be clear enough that both your engineering-minded CEO and your external auditor can read the trial balance without confusion. We recommend grouping revenue accounts by delivery type: subscription revenue, transaction fee revenue, and professional services revenue. On the liability side, you'll need dedicated accounts for client trust funds and security deposit obligations. Cost accounts should separate platform hosting from real estate data licensing, since they behave differently during due diligence. Keep your numbering system flexible enough to add sub-accounts as you launch new product lines.

Here are five accounts commonly added for PropTech companies:

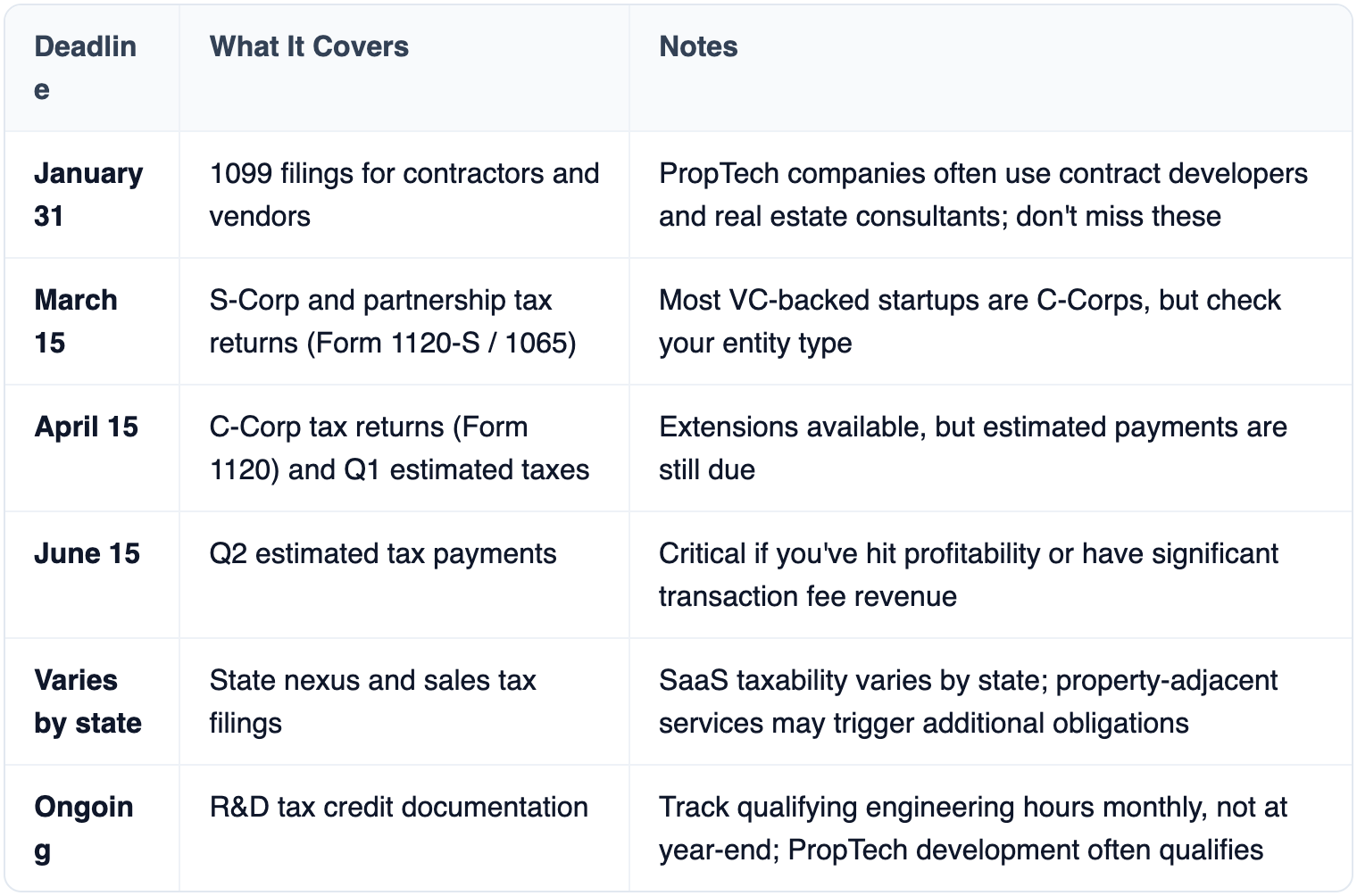

PropTech startups face tax considerations that go beyond the standard startup checklist. If your platform operates across multiple states, you likely have nexus obligations tied to where your real estate clients or their properties are located, not just where your employees sit. R&D tax credits also play a big role here, since much of your engineering work may qualify under Section 41.

Choosing the right accounting platform is essential for PropTech startups. Here's what to prioritize:

Do PropTech startups need a specialized accountant, or can any startup CPA handle it?

A general startup CPA can handle basics like payroll and tax filings. But PropTech-specific issues like trust accounting, multi-stream revenue recognition, and real estate compliance require someone who's worked in the space. An accounting firm with PropTech or real estate tech clients will save you from costly reclassifications during audits.

When should a PropTech startup hire a full-time accountant versus outsourcing?

At the seed stage, outsourcing to a fractional CFO or accounting firm makes sense. You don't have enough transaction volume to justify a full-time hire. Once you're past Series A and processing significant payment volume or managing trust accounts, bringing someone in-house becomes worth it. The trigger is usually complexity, not revenue.

How should PropTech startups handle R&D tax credits?

Track qualifying activities from day one. Engineering time spent on building new features, improving algorithms, or integrating with real estate data systems often qualifies under Section 41. Keep contemporaneous records: timesheets, project descriptions, and technical documentation. Retroactive reconstruction is expensive and less defensible.

What's the biggest accounting mistake PropTech founders make?

Treating all revenue as a single line item. If you bundle subscriptions, transaction fees, and services into one number, you'll face problems during due diligence. Investors want to see recurring versus transactional revenue separated cleanly. Fix this early, because reclassifying two years of revenue data is painful.

Are there specific sales tax rules for PropTech platforms?

Yes, and they're complicated. SaaS taxability varies by state. If your platform also provides services that touch physical property, like maintenance coordination or property management, those services may be taxed differently than pure software. Get a nexus study done once you're operating in more than five states.

Getting your accounting right from the start isn't just about compliance. It's about building a company that investors trust, auditors approve, and acquirers want to buy. The PropTech space is maturing fast in 2026, and financial discipline separates the startups that scale from those that stall.

Start with a chart of accounts that reflects your actual business model. Set up trust accounting properly if you touch client funds. Track R&D hours monthly. Separate your revenue streams before your first audit, not after.

If you're a founder, find an accounting partner who knows both SaaS metrics and real estate financial mechanics. If you're an accountant advising PropTech clients, invest the time to understand their product and payment flows deeply. The companies that get this right build credibility with every financial statement they produce. That credibility compounds, just like the interest on the trust accounts you're managing.