Running a media startup means juggling creative ambitions with financial reality. Revenue doesn't always arrive on a predictable schedule. Costs pile up in ways that look nothing like a typical SaaS or retail business. And the accounting rules that govern content creation, licensing, and distribution can trip up even experienced founders. Whether you're building a podcast network, a digital publishing platform, or a video production studio, your books need to reflect the unique economics of media. This guide to accounting for media startups breaks down the specific challenges, structures, and strategies you'll need to stay financially healthy from day one through Series A and beyond. Think of it as the financial playbook your creative team didn't know it needed.

Accounting for media startups is the practice of tracking, categorizing, and reporting financial activity in a business built around content creation, distribution, or licensing. It matters because media companies earn and spend money in patterns that standard accounting frameworks don't always handle well.

Here are the three most important things to know:

Even if you read nothing else, remember this: treat your content like inventory, your revenue streams like separate product lines, and your cash flow projections like a living document you revisit weekly.

Your clients in the media space face financial realities that most small business accounting frameworks weren't designed for. The first major difference is content capitalization. When a media startup spends $80,000 producing a documentary series, that cost isn't simply an expense in the month it's paid. Under ASC 926 and related guidance, production costs for content with a determinable future revenue stream should be capitalized and amortized. The amortization method often follows an individual-film-forecast model, meaning you're matching expense recognition to projected revenue curves. Getting this wrong overstates early losses or, worse, inflates profitability.

The second nuance is multi-stream revenue allocation. A single piece of content might generate ad revenue, subscription fees, licensing income, and merchandise sales. Each stream triggers different recognition timing. A licensing deal signed in March with delivery in June and payment in September creates three distinct accounting events. Your clients need systems that track these separately, not lump them into a single "revenue" line.

Third, media startups frequently operate with project-based cost structures rather than steady operational spending. One quarter might involve minimal costs while the next sees a $200,000 production sprint. This volatility makes traditional monthly financial comparisons misleading without proper context and normalization.

A standard chart of accounts won't capture the financial activity that defines a media business. You'll need dedicated accounts that separate content production costs from general operating expenses, distinguish between different revenue streams, and track IP-related assets distinctly. Naming conventions matter here: investors and lenders expect to see production costs broken out clearly, not buried inside a generic "cost of goods sold" line. Your chart should also accommodate project-level tracking, since many media startups need to report profitability by show, series, or publication rather than just at the company level. We recommend building your chart with expansion in mind. A podcast startup today might add video production next year, and your account structure should handle that without a full rebuild.

Here are five accounts commonly added for media companies:

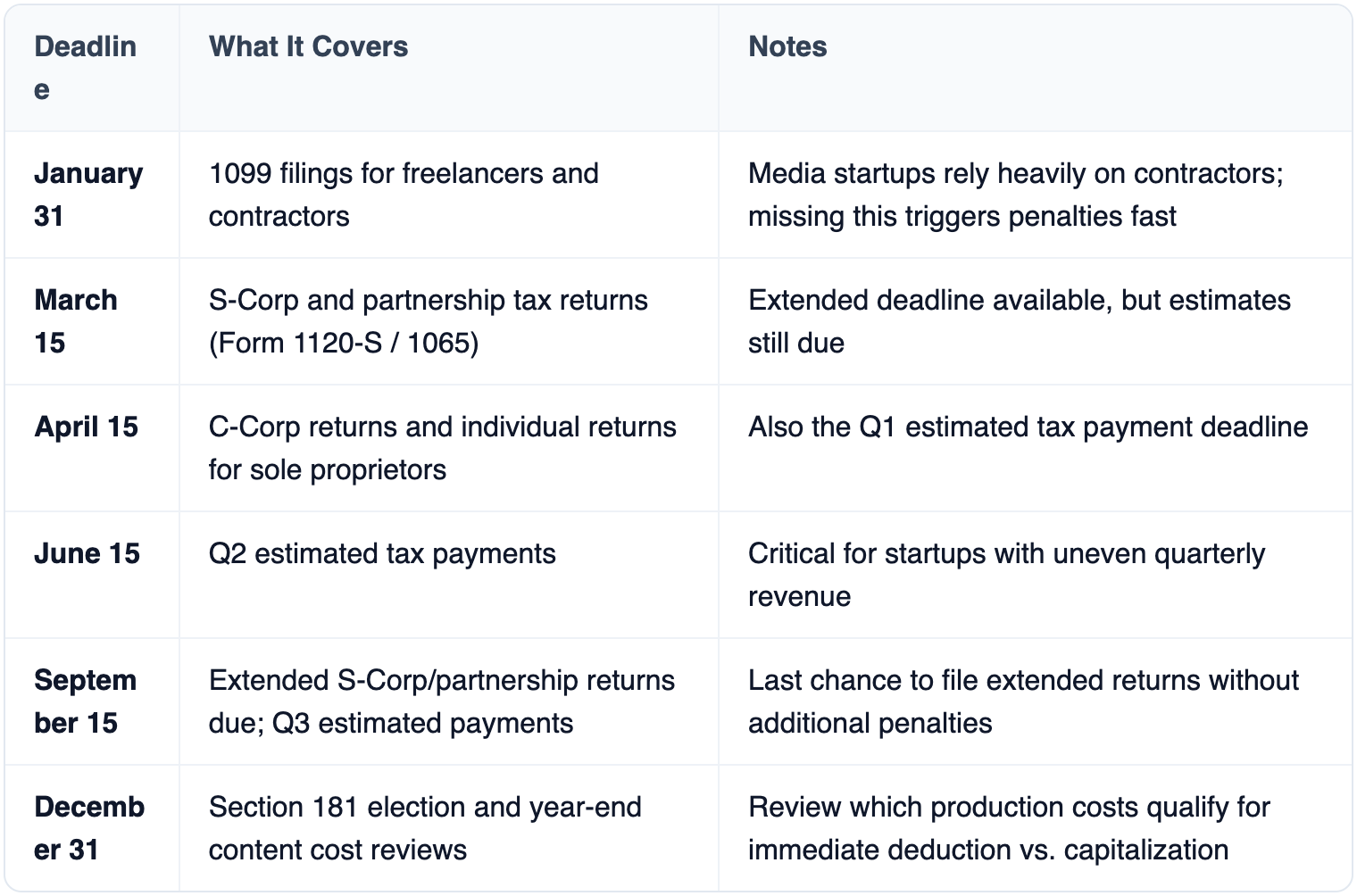

Media startups face a few tax wrinkles that other industries don't. State tax nexus is a big one: if your content is consumed or your freelancers are located across multiple states, you may owe taxes in jurisdictions you've never visited. Section 181 and its successors also allow certain production costs to be deducted immediately rather than capitalized, which can significantly affect your tax bill in high-spending years.

Not every accounting platform handles the financial complexity of a media business. Here's what to prioritize:

Do I need a specialized accountant for my media startup, or can any CPA handle it?

Any licensed CPA can technically do your books. But media accounting involves content capitalization rules, multi-stream revenue recognition, and IP valuation that most generalist firms rarely encounter. A firm with media clients will set up your chart of accounts correctly from day one and prevent costly reclassifications later. The difference shows up most during audits and fundraising due diligence.

How should a seed-stage media startup handle content production costs?

At the seed stage, keep it simple but structured. Track all production costs by project from the start, even if you're expensing everything initially. Once you have content generating recurring revenue, you'll want to capitalize those costs and amortize them. Building the tracking habit early saves you from a painful retroactive cleanup when your Series A investors ask for audited financials.

Should I recognize sponsorship revenue when I receive payment or when the campaign runs?

You recognize it as the campaign runs, not when the check arrives. If a sponsor pays $60,000 in January for a campaign running January through March, you book $20,000 per month. The remaining balance sits on your balance sheet as deferred revenue. This is a core ASC 606 requirement, and getting it wrong is one of the most common mistakes we see in early-stage media companies.

What's the biggest financial mistake media startups make?

Treating all content spending as a current-period expense. This approach understates your assets, overstates your losses, and makes your company look less valuable than it is. If your content has a useful life beyond the current period, a portion of that cost belongs on your balance sheet. Work with your accountant to establish a clear capitalization policy early.

How often should a media startup review its financials?

Monthly, at minimum. But weekly cash flow reviews are essential for media startups because of the gap between production spending and revenue collection. A monthly P&L tells you where you've been. A weekly cash flow forecast tells you whether you can afford next month's production schedule.

Getting your accounting right isn't just about compliance. It's about building a financial foundation that supports creative risk-taking. The media startups that scale successfully are the ones that understand their unit economics by project, forecast cash flow with precision, and present clean financials to investors without scrambling.

Start by auditing your current chart of accounts against the recommendations above. Set up project-level cost tracking if you haven't already. And if your current accountant has never handled content capitalization or multi-stream revenue recognition, it's time to find one who has. Your creative vision deserves a financial structure that can keep up with it. Don't wait until your Series A to discover your books need a complete overhaul; build the right system now, and you'll thank yourself later.