Running a healthcare startup means juggling clinical innovation, regulatory compliance, and investor expectations all at once. Your accounting system has to keep pace with each of those demands, or you'll find yourself scrambling during audits, fundraising rounds, or tax season. This guide to accounting for healthcare startups breaks down the financial practices that separate thriving companies from those that stall out. Whether you're pre-revenue or scaling past Series A, the principles here apply. We built this resource from real patterns we see across dozens of healthcare clients, not from generic advice you could find in any small business handbook. If your books aren't structured for the unique pressures of healthcare, you're building on a shaky foundation. The good news: getting this right isn't as complicated as it seems. It just requires knowing where healthcare accounting diverges from the standard playbook, and acting on that knowledge early. Stick around for the specific frameworks, deadlines, and evaluation criteria that matter most for your startup's financial health.

Healthcare startup accounting is the practice of tracking, reporting, and managing finances within a company that operates under healthcare-specific regulations, reimbursement models, and compliance requirements. It matters because a single misclassification of revenue or a missed compliance filing can trigger penalties, delay funding, or attract unwanted regulatory attention.

Here are the three most important things to know:

Even if you read nothing else, those three points will save you from the most common financial missteps we see in this space.

From an accounting firm's perspective, healthcare clients require a fundamentally different approach than a typical tech or e-commerce startup. The first major distinction is the reimbursement cycle. Your clients in this space don't just invoice a customer and collect payment. They submit claims to insurers, Medicare, or Medicaid, then wait 30 to 90 days for adjudication. Denied claims create accounts receivable complications that demand specialized tracking and follow-up workflows.

The second distinction is regulatory expense layering. A standard startup might spend on software, payroll, and marketing. Healthcare startups carry additional cost layers for HIPAA compliance audits, clinical credentialing, malpractice coverage, and sometimes FDA submission fees. These aren't one-time costs; they recur and fluctuate. Your chart of accounts, your expense categories, and your forecasting models all need to reflect this reality.

Finally, there's the matter of grant and research funding. Many healthcare startups receive NIH grants, SBIR awards, or other restricted funds. These come with strict reporting requirements and spending restrictions. Commingling restricted and unrestricted funds is a serious compliance risk that generic accounting setups simply aren't designed to prevent.

A healthcare startup's chart of accounts looks noticeably different from a standard tech company's. You'll need dedicated revenue accounts for each payer type: commercial insurance, Medicare, Medicaid, self-pay patients, and contract or subscription revenue from provider clients. On the expense side, expect to add accounts for HIPAA compliance costs, clinical credentialing fees, malpractice insurance, and regulatory submission expenses. Many startups also need a separate account for bad debt related to denied or underpaid claims, which behaves differently from typical bad debt because denial rates follow payer-specific patterns. Naming conventions matter here too. We recommend prefixing clinical expense accounts with "CL-" and compliance accounts with "COMP-" so your team can quickly filter reports by category. This small habit pays off during audits and board reporting.

Example accounts to consider:

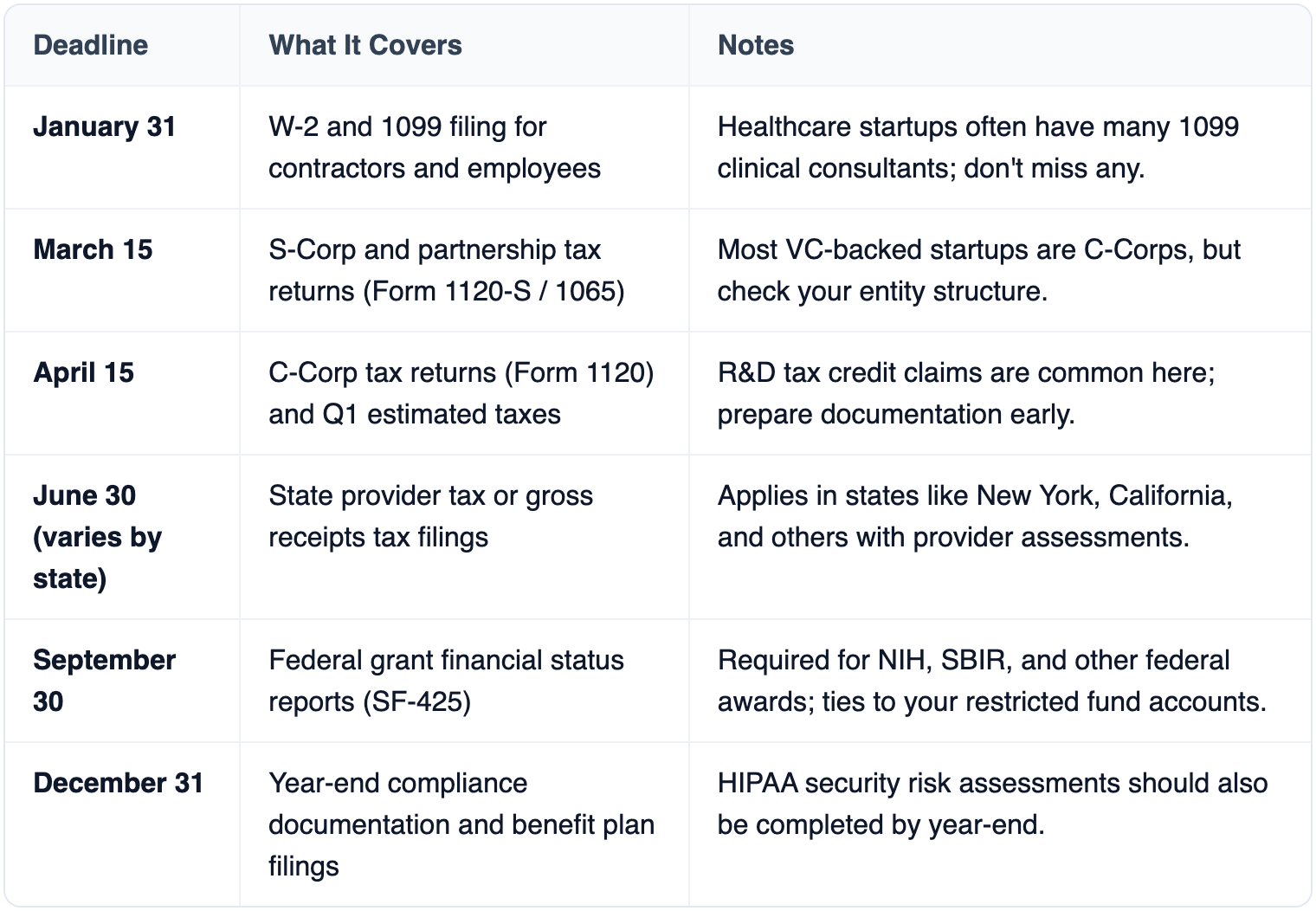

Healthcare startups face a tax calendar that blends standard business deadlines with sector-specific obligations. State-level provider taxes, gross receipts assessments on medical services, and grant reporting cycles all layer on top of the usual federal filings. Missing any of these can trigger penalties or jeopardize your funding.

Plan your calendar around these dates. One missed grant report can freeze your next disbursement.

Not every accounting platform fits a healthcare startup's needs. Here's what to prioritize when you're evaluating your options:

Do healthcare startups need a specialized accounting firm?

Yes, in most cases. A generalist firm won't catch healthcare-specific issues like improper revenue recognition on insurance claims, misclassified grant expenses, or state provider tax obligations. Look for firms with healthcare clients on their roster and ask about their experience with HIPAA-related financial workflows.

When should a healthcare startup hire a full-time accountant versus outsourcing?

At the seed stage, outsourcing to a firm that knows healthcare accounting is usually the smarter move. You get specialized expertise without the overhead of a full-time hire. Once you're past Series A and processing a high volume of claims or managing multiple grants, bringing someone in-house starts to make sense. The tipping point is typically when monthly transaction volume exceeds what a part-time engagement can handle efficiently.

How does the R&D tax credit apply to healthcare startups?

Many healthcare startups qualify for the federal R&D tax credit under Section 41. If you're developing new medical devices, software for clinical use, or novel treatment protocols, your development expenses likely qualify. Startups with less than $5 million in gross receipts can apply the credit against payroll taxes, which is valuable when you're pre-revenue.

What's the biggest accounting mistake healthcare startups make?

Treating compliance and regulatory costs as miscellaneous expenses. When these costs aren't tracked in dedicated accounts, you lose visibility into a major spending category. This makes budgeting unreliable and creates problems during due diligence when investors want to understand your cost structure.

Should we use cash basis or accrual basis accounting?

Accrual basis, almost always. Healthcare revenue cycles involve significant time gaps between service delivery and payment collection. Cash basis accounting would dramatically misrepresent your financial position in any given month. Investors and lenders expect accrual-based financials, and GAAP requires it once you reach a certain size.

Getting your accounting right from the start isn't just about avoiding mistakes. It's about building a system that supports fundraising, passes audits cleanly, and gives you real-time insight into your financial position. Healthcare startups that treat accounting as an afterthought inevitably spend more time and money fixing problems later.

Start with a healthcare-specific chart of accounts. Set up restricted fund tracking before you receive your first grant dollar. Choose software that handles multi-payer complexity. And work with an accounting partner who genuinely understands the healthcare sector's unique demands.

The startups we see succeed financially aren't the ones with the most funding. They're the ones whose books tell a clear, accurate, and compliant story from day one. Your accounting system is the backbone of that story. Build it well, and every other financial decision gets easier.