Hardware startups face a unique financial reality. You're not just tracking subscriptions and payroll. You're managing raw materials, manufacturing partners, customs duties, and inventory sitting in warehouses across multiple countries. The accounting demands are fundamentally different from those of a SaaS company, and getting them wrong early can cost you a funding round or worse.

That's why understanding accounting for hardware startups isn't optional: it's survival. Whether you're building your first prototype or scaling production after a Series A, your books need to reflect the physical complexity of your business. Most generic accounting advice falls short here. Hardware founders need a financial framework built around atoms, not just bits. This guide breaks down the specific challenges, structures, and strategies that hardware companies need to get right from day one. If you're a founder, CFO, or accounting professional serving this space, the next few minutes could save you months of cleanup later.

Accounting for hardware startups is the practice of tracking, categorizing, and reporting financial activity for companies that design and sell physical products. It matters because hardware businesses carry inventory, manage complex supply chains, and face cost-of-goods-sold calculations that software companies never deal with.

Here are the three most important things to know:

Get these three right, and you're ahead of 90% of hardware startups at your stage.

If you're an accounting professional with clients building physical products, you already know the books look nothing like a typical tech startup. The biggest difference is inventory. A SaaS company's primary assets are people and code. A hardware company's balance sheet carries raw materials, partially assembled units, and finished goods: each requiring distinct treatment under GAAP or IFRS. You need to track inventory across multiple locations, sometimes across borders, and reconcile it against purchase orders, shipping documents, and manufacturing reports.

The second major difference is revenue recognition timing. Your clients might ship products with extended payment terms, offer warranties, or bundle hardware with software subscriptions. Each scenario triggers different recognition rules. A unit shipped FOB origin has a different recognition point than one shipped FOB destination. Getting this wrong isn't just sloppy: it can trigger restatements that destroy investor confidence.

Cost allocation is the third area that trips up firms new to this space. Tooling costs, mold development, NRE (non-recurring engineering) fees, and certification testing all need proper capitalization or expensing treatment. The rules aren't intuitive, and your clients will push back on anything that hits their P&L before they're generating revenue.

Your chart of accounts should reflect the physical nature of your business from the start. Most standard templates are built for service or software companies, so you'll need to add accounts that capture inventory at multiple stages, manufacturing overhead, and landed costs. Naming conventions matter too: your accounts should distinguish between raw materials inventory, work-in-progress inventory, and finished goods inventory rather than lumping everything under a single "Inventory" line. Freight-in, customs duties, and packaging materials each deserve their own expense or COGS sub-account. If you're outsourcing manufacturing, create a separate account for contract manufacturing fees so you can track them independently from your internal labor costs. This granularity pays off during due diligence when investors want to understand your true unit economics.

Here are five accounts you'll likely need that most templates don't include:

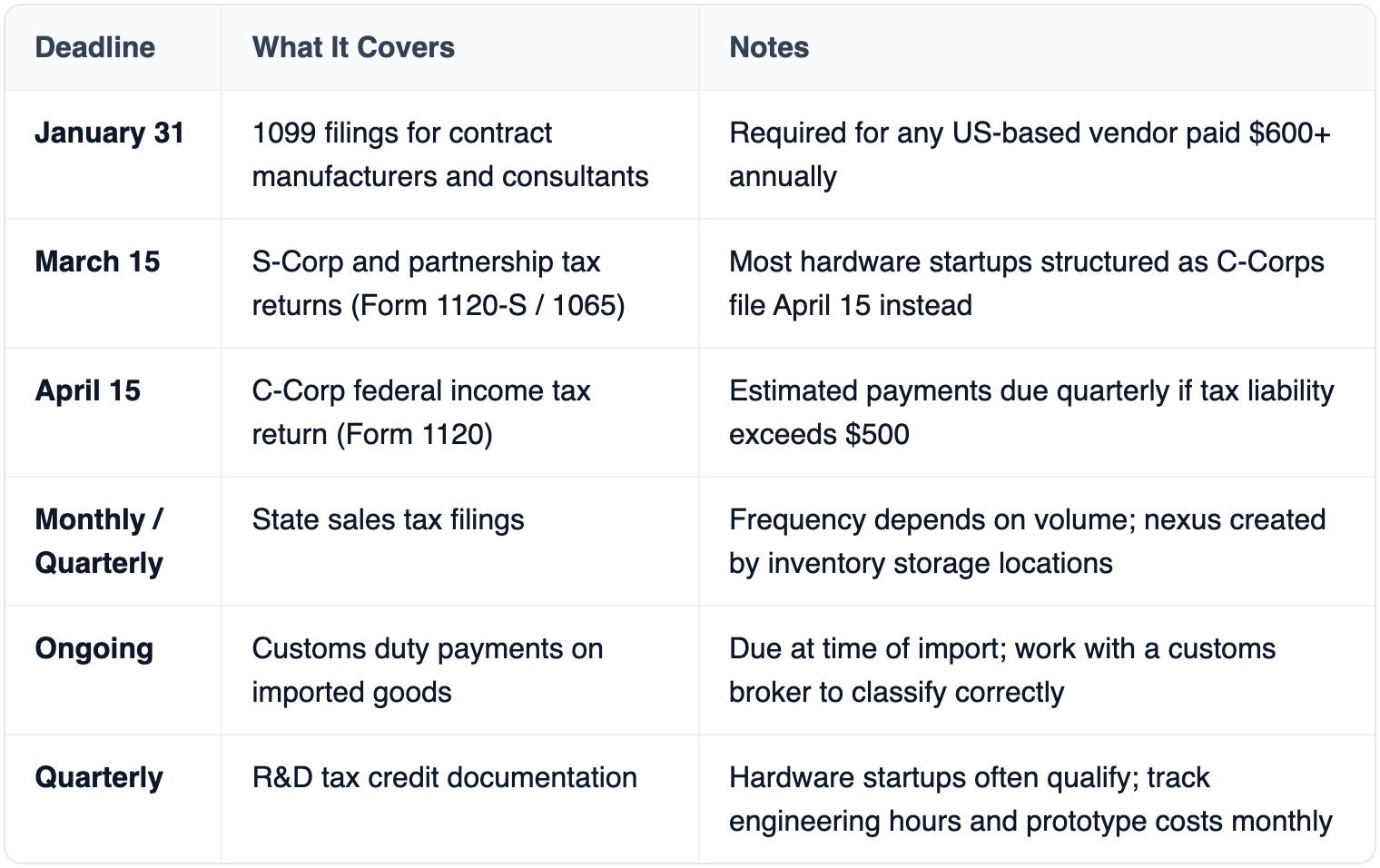

Hardware startups face tax obligations that go well beyond standard income filing. Importing physical goods triggers customs duties, and selling across state lines (or internationally) creates sales tax and VAT obligations that compound quickly. If you're holding inventory in a third-party warehouse in another state, you likely have nexus there: and that means filing obligations you might not expect.

Not every accounting platform handles physical product businesses well. Here's what to prioritize:

Do hardware startups need a specialized accounting firm?

Yes, in most cases. A firm experienced with physical product companies will understand inventory accounting, COGS complexity, and import/export tax issues from the start. General-practice firms often miscategorize manufacturing costs or miss sales tax nexus obligations, which creates expensive problems during audits or fundraising due diligence.

Should I use accrual or cash basis accounting?

Accrual basis. Full stop. Hardware startups pay for inventory months before selling it. Cash basis accounting will make your financials look wildly inconsistent from month to month. Investors expect accrual-based financials, and you'll need them for any Series A or later fundraise.

How should seed-stage hardware startups handle prototype costs?

Prototype costs before you have a commercially viable product are typically expensed as R&D. Once you're producing units for sale, manufacturing costs shift to inventory (an asset) and hit COGS only when units are sold. The transition point matters: document it clearly.

What's the biggest accounting mistake hardware founders make?

Underestimating their true cost per unit. Founders often calculate COGS using only component costs and assembly fees. They forget to include freight, duties, packaging, quality testing, scrap rates, and warranty costs. This inflated margin looks great in a pitch deck until an experienced investor asks for a full landed cost breakdown.

How often should hardware startups reconcile inventory?

Monthly at minimum. If you're shipping more than 500 units per month, consider cycle counting: a process where you verify a portion of inventory each week rather than doing a single massive count. Discrepancies between your books and physical inventory are inevitable. Catching them early prevents write-offs that shock your P&L.

Hardware accounting isn't harder than software accounting: it's just different. The physical nature of your product creates financial complexity in inventory, COGS, taxes, and cash flow that most generic advice ignores. The founders who succeed financially aren't the ones with the best products. They're the ones who understand their unit economics, track costs at a granular level, and build financial systems that scale with production volume.

Start by setting up your chart of accounts correctly. Choose accounting software that handles inventory in stages. Work with a firm or advisor who's done this before: ideally one with hardware clients at your stage. And reconcile your inventory monthly, no exceptions.

Your accounting is the financial language investors, partners, and acquirers use to evaluate your business. Make sure it tells an accurate story. The companies that treat their books as a strategic asset, not a compliance chore, are the ones that raise capital faster and operate with confidence.