Fintech is one of the fastest-growing startup verticals globally. It's also one of the hardest to get right from an accounting perspective. Between regulatory scrutiny, complex revenue models, and the constant movement of digital funds, your books need to be airtight from day one. If you're a founder building a payments app, a neobank, or a lending platform, getting your financial house in order isn't optional. It's survival. This guide to accounting for fintech startups covers the specific challenges, structures, and strategies that separate this vertical from every other industry. Whether you're pre-seed or scaling past Series A, the principles here apply. Think of this as your financial operating manual: practical, specific, and built for the realities of fintech in 2026.

Fintech accounting is the practice of tracking, classifying, and reporting financial activity for startups that handle, move, or facilitate money as their core product. It matters because regulators, investors, and banking partners all demand a higher standard of financial transparency from companies that touch consumer funds.

Here are the three most important things to know:

Even if you read nothing else, those three points will shape how you think about your books.

From an accounting firm's perspective, fintech clients require a fundamentally different approach than a typical SaaS or e-commerce startup. The reason is simple: your clients in this space are regulated like financial institutions but structured like tech companies. That tension creates accounting complexity you won't find in other verticals.

First, there's the issue of fund segregation. Most startups have one pool of cash: their own. Fintech startups often hold customer deposits, pending transfers, or loan collateral alongside their operating funds. Your chart of accounts and bank reconciliation processes need to reflect this separation clearly, or you risk both regulatory violations and misstated financials.

Second, fintech revenue doesn't behave like traditional subscription revenue. A payments company might earn fractions of a cent per transaction across millions of events daily. A lending platform recognizes interest income over the life of a loan, not at the point of sale. These aren't edge cases. They're the core business model, and your accounting system has to handle them with precision from the earliest stages.

A standard startup chart of accounts won't work for fintech. You need accounts that reflect the unique flow of funds through your business. Most critically, you'll want separate liability accounts for customer funds held in trust or escrow. These are not your assets, and they shouldn't appear as such on your balance sheet. Your revenue accounts also need granularity: splitting interchange income, subscription fees, interest earned on float, and late payment penalties into distinct categories gives you and your investors a clear picture of where money actually comes from.

Naming conventions matter too. Auditors and regulators expect to see industry-standard terminology. "Customer trust account" means something specific. "Misc. deposits" does not. Build your chart of accounts with future audits in mind, not just your current bookkeeping needs.

Here are a few example accounts common in fintech:

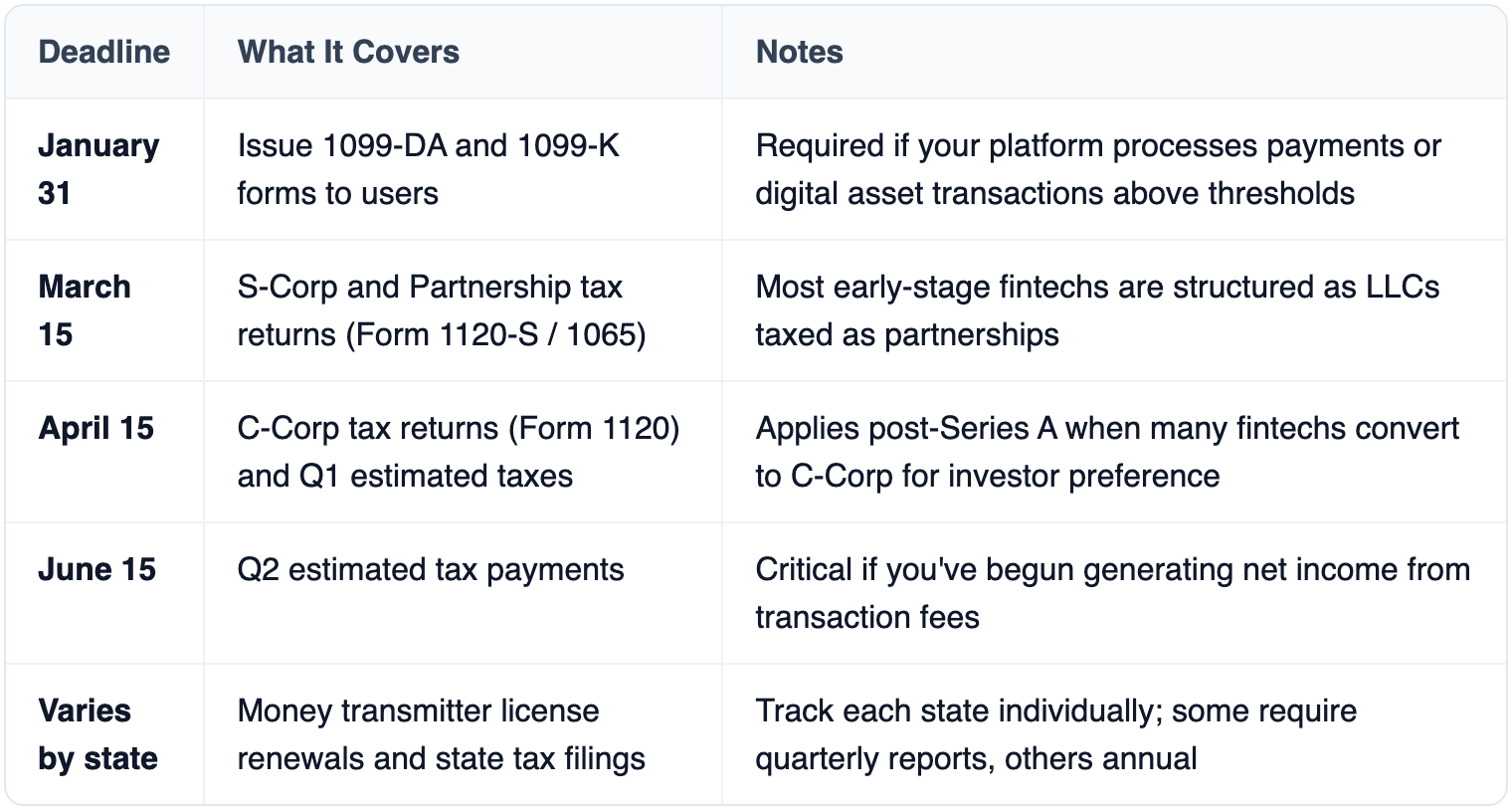

Fintech startups face a tax environment shaped by multi-state operations, digital asset rules, and financial services regulations. If you're operating across state lines, which most payment and lending platforms are, you likely have nexus in multiple jurisdictions. That means multiple filing obligations, each with its own deadlines and rules.

The 2025 IRS updates to digital asset reporting requirements (Form 1099-DA) now apply in full for the 2026 tax year. If your platform facilitates any crypto transactions, you're responsible for issuing these forms and tracking cost basis for users.

Not every accounting platform can handle fintech's unique demands. Here's what to prioritize when choosing yours.

Do fintech startups need a specialized accounting firm?

Yes, in most cases. A generalist firm may not understand fund segregation, multi-state money transmitter compliance, or the nuances of ASC 606 as it applies to transaction-based revenue. Look for firms with direct fintech or financial services experience. Ask them how many fintech clients they currently serve and whether they've handled regulatory audits in the space.

What accounting method should a fintech startup use?

Accrual basis, almost without exception. Cash basis accounting can't accurately represent the timing of fintech revenue and expenses. If you earn interchange fees on transactions processed today but settled three days later, accrual accounting captures that correctly. Investors and auditors expect accrual-based financials, especially once you're past the seed stage.

How should a seed-stage fintech handle accounting?

Keep it simple but structured. Set up your chart of accounts correctly from the start, even if transaction volume is low. Use cloud-based accounting software with API integrations. Hire a part-time bookkeeper or outsourced CFO who understands fintech. The cost of fixing a messy financial foundation later is always higher than setting it up right now.

When should a fintech startup get its first audit?

Most fintech startups face their first audit demand around Series A or when they apply for certain banking partnerships. Some state regulators require audited financials as part of money transmitter licensing. Don't wait until the request comes in. Start preparing by maintaining clean books, documented internal controls, and reconciled accounts from month one.

How do fintech startups account for loan losses?

If you're a lending platform, you need to establish an allowance for loan losses based on expected credit losses under the CECL model (ASC 326). This means estimating future losses at the time of loan origination, not waiting until a borrower defaults. It's a forward-looking model that requires data, assumptions, and regular updates to your reserve calculations.

Getting accounting right as a fintech startup isn't just about compliance. It's about building a company that investors trust, regulators approve, and banking partners want to work with. The principles in this guide to fintech startup accounting apply whether you're processing your first thousand transactions or your first billion.

Start with a clean chart of accounts. Separate customer funds from day one. Choose software that matches your transaction volume. And work with advisors who understand the specific demands of financial services.

Your books tell the story of your business. Make sure they're telling the right one. If you're unsure where your accounting stands today, get a professional review before your next funding round or regulatory filing. The earlier you invest in financial clarity, the fewer surprises you'll face when it matters most.