EdTech is booming. Global spending on education technology is projected to exceed $400 billion by 2027, and thousands of new startups enter the space each year. But behind every promising learning platform or AI tutoring tool sits a set of financial books that need careful attention. EdTech companies face a unique mix of revenue models, regulatory requirements, and cost structures that generic accounting advice simply doesn't cover. Whether you're a founder bootstrapping a K-12 app or a CFO at a Series A company scaling internationally, your accounting setup will make or break your ability to raise capital, stay compliant, and grow sustainably. This guide to accounting for EdTech startups breaks down everything you need to know: from chart of accounts specifics to tax deadlines, software selection, and the most common pitfalls we see firms stumble into. Think of it as the financial playbook your EdTech company deserves but probably doesn't have yet. The advice here is written from the perspective of accountants who work with education technology companies daily, so you're getting practical guidance, not theory.

Accounting for EdTech startups is the process of tracking, reporting, and managing the financial activity unique to education technology companies. It matters because EdTech revenue models, cost structures, and compliance requirements differ sharply from those of typical SaaS or consumer tech businesses.

Here are the three most important things to know:

Even if you stop reading here, those three areas deserve your immediate attention.

EdTech sits at the intersection of two heavily regulated worlds: education and technology. That overlap creates accounting nuances your clients won't encounter in standard SaaS.

First, revenue streams are unusually fragmented. A single EdTech company might earn money from B2C subscriptions, B2B district-wide licenses, per-seat institutional pricing, freemium upgrades, and grant-funded pilot programs, all at once. Each stream has different recognition rules, billing cycles, and refund policies. Treating them uniformly is a fast path to a restatement.

Second, the customer base introduces procurement complexity. School districts and universities operate on fiscal year calendars that rarely align with a startup's own fiscal year. Purchase orders often arrive months before services begin, and payment can lag 60 to 120 days. Your accounts receivable aging reports will look nothing like a typical B2B SaaS company's.

Third, compliance reporting for publicly funded customers adds a layer most startups aren't prepared for. If your client's product touches Title I, IDEA, or E-Rate funding, their books need to support audits that trace every dollar back to its source.

Your chart of accounts is the skeleton of your financial reporting. For EdTech companies, the standard SaaS chart of accounts needs meaningful modifications. You'll want separate revenue accounts for each distinct income stream: subscriptions, implementation services, professional development, and content licensing should never be lumped together. On the expense side, you need granular tracking of content development costs separate from platform engineering costs, because they follow different capitalization rules. Hosting and infrastructure costs also deserve their own line items, since gross margin calculations for investor reporting depend on isolating cost of revenue from general R&D. Naming conventions matter too. If you're selling to school districts, your chart should mirror the language used in education procurement so your invoices and financial reports align with how your customers categorize spending.

Common accounts to add:

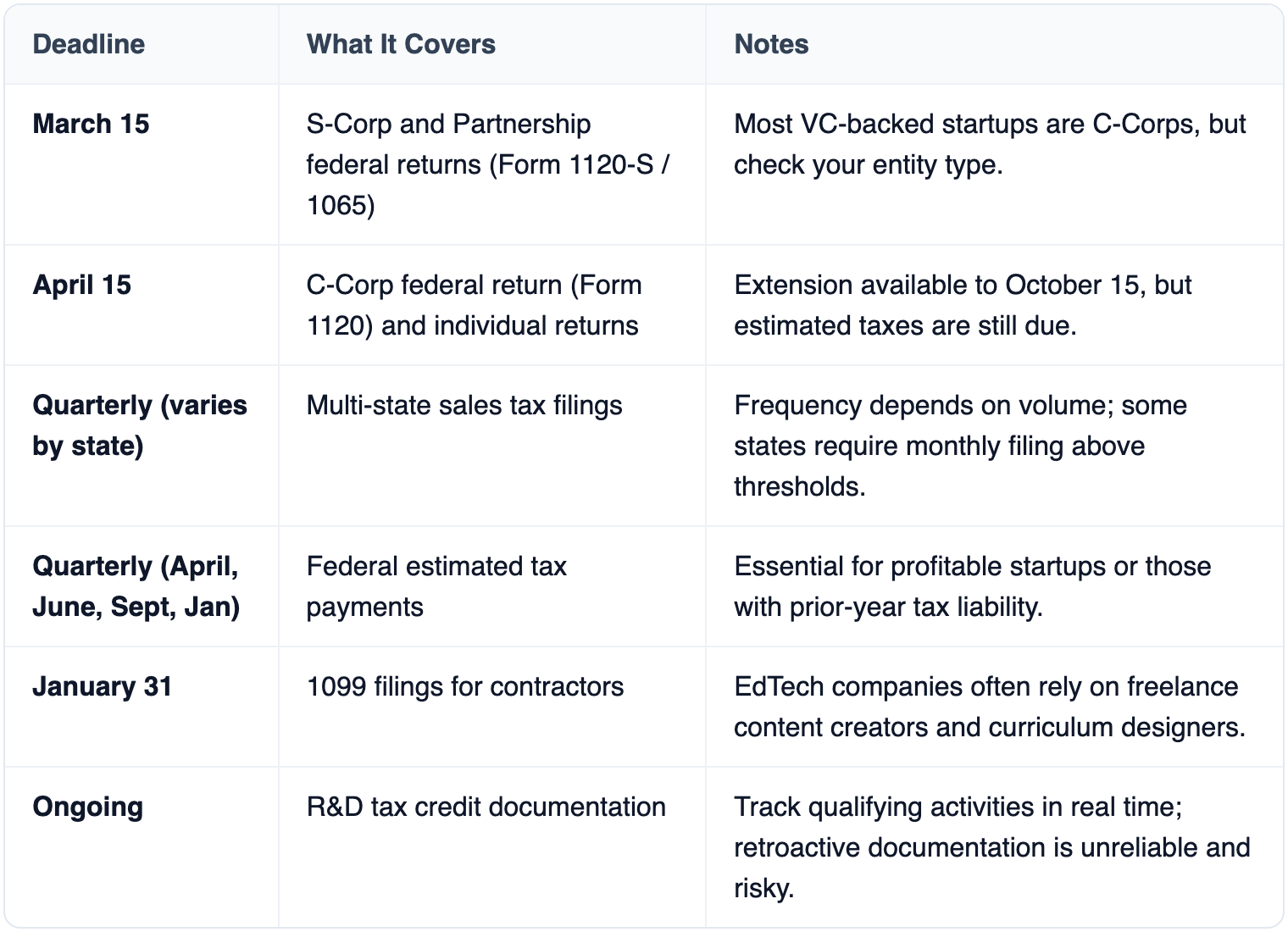

EdTech startups face a tax environment shaped by multi-state sales, R&D-heavy operations, and the unique exemptions that come with selling to educational institutions. Many states exempt sales to public schools but not private ones, and the definition of "educational software" for tax purposes varies. Missing a filing deadline or misclassifying an exemption can result in penalties that hit a startup's cash flow hard.

Not every accounting platform fits the needs of an education technology company. Here's what to prioritize:

Do EdTech startups qualify for the R&D tax credit?

Yes, most do. Building educational software, developing adaptive learning algorithms, and creating interactive content all typically qualify as research activities under IRC Section 41. Startups with less than $5 million in gross receipts can apply the credit against payroll taxes, which is especially valuable for pre-revenue companies. Document your qualifying activities monthly, not at year-end.

Should a seed-stage EdTech startup hire an accountant or use DIY software?

At the seed stage, a hybrid approach works best. Use accounting software for day-to-day bookkeeping, but engage an accountant or accounting firm with EdTech experience for quarterly reviews, tax filings, and entity structuring. The cost of fixing early mistakes far exceeds the cost of professional guidance from the start.

How should EdTech companies handle revenue from pilot programs?

Pilot programs with school districts often involve discounted or free access. If there's no payment, there's no revenue to recognize, but you should still track the costs associated with pilots separately. If the pilot includes a paid component, recognize revenue based on the same ASC 606 principles you'd apply to any other contract.

What's the biggest accounting mistake EdTech startups make before a Series A raise?

Inconsistent revenue recognition. Investors and their due diligence teams will scrutinize how you've recognized revenue from bundled contracts. If you've been recognizing all revenue at the point of sale rather than over the service period, you'll face a painful restatement that can delay or kill a funding round.

Why should EdTech companies work with a specialized accounting firm?

Generic accountants often miss the nuances of education procurement cycles, grant compliance, and multi-element revenue arrangements. A firm experienced in EdTech understands how school district budgets work, knows which states exempt educational software from sales tax, and can structure your financials in the format investors in the education sector expect to see.

Getting your accounting right isn't glamorous, but it's the foundation everything else rests on: fundraising, pricing decisions, tax savings, and compliance. The EdTech companies that treat accounting as a strategic function rather than an afterthought consistently outperform those that don't.

Start with three actions this week. First, audit your revenue recognition practices against ASC 606 and fix any bundled contracts that aren't properly allocated. Second, review your chart of accounts and add the granular categories your business actually needs. Third, if you're approaching a fundraise, bring in an accounting firm that knows the education technology space before investors start asking questions you can't answer.

Your books tell the story of your company. Make sure they're telling the right one.