Running an online store is exciting until tax season hits. Then, the thrill of growing sales can quickly turn into confusion over multi-state obligations, inventory valuation, and payment processor fees buried in your books. E-commerce accounting isn't the same as accounting for a local service business, and treating it that way is one of the fastest paths to financial trouble for a young company. Whether you're bootstrapping from your garage or preparing for a seed round, getting your financial house in order early pays dividends for years. This guide to accounting for e-commerce startups breaks down the unique challenges, the tools you'll need, and the deadlines you can't afford to miss. Consider it your financial playbook for selling online.

E-commerce accounting is the process of tracking, categorizing, and reporting every financial transaction tied to an online retail business. It matters because inaccurate books lead to tax penalties, cash flow surprises, and failed fundraising rounds. Here are the three most important things to know:

Get these three things right, and you're ahead of most early-stage online sellers.

If you're advising clients in this space, the first thing to understand is that e-commerce businesses generate a high volume of low-dollar transactions across multiple channels. A brick-and-mortar shop might process 50 sales a day through one register. An online store might process 500 orders a day through Shopify, Amazon, and its own website, each with different fee structures, refund policies, and settlement timelines. Reconciling these channels is a daily exercise, not a monthly one.

The second major difference is inventory complexity. Your clients aren't just buying and selling goods. They're dealing with landed costs that include shipping from overseas suppliers, customs duties, and warehousing fees. Each of these components affects cost of goods sold (COGS), and getting COGS wrong distorts every profitability metric downstream. A service business doesn't face this. A SaaS company doesn't face this. It's a distinctly e-commerce problem.

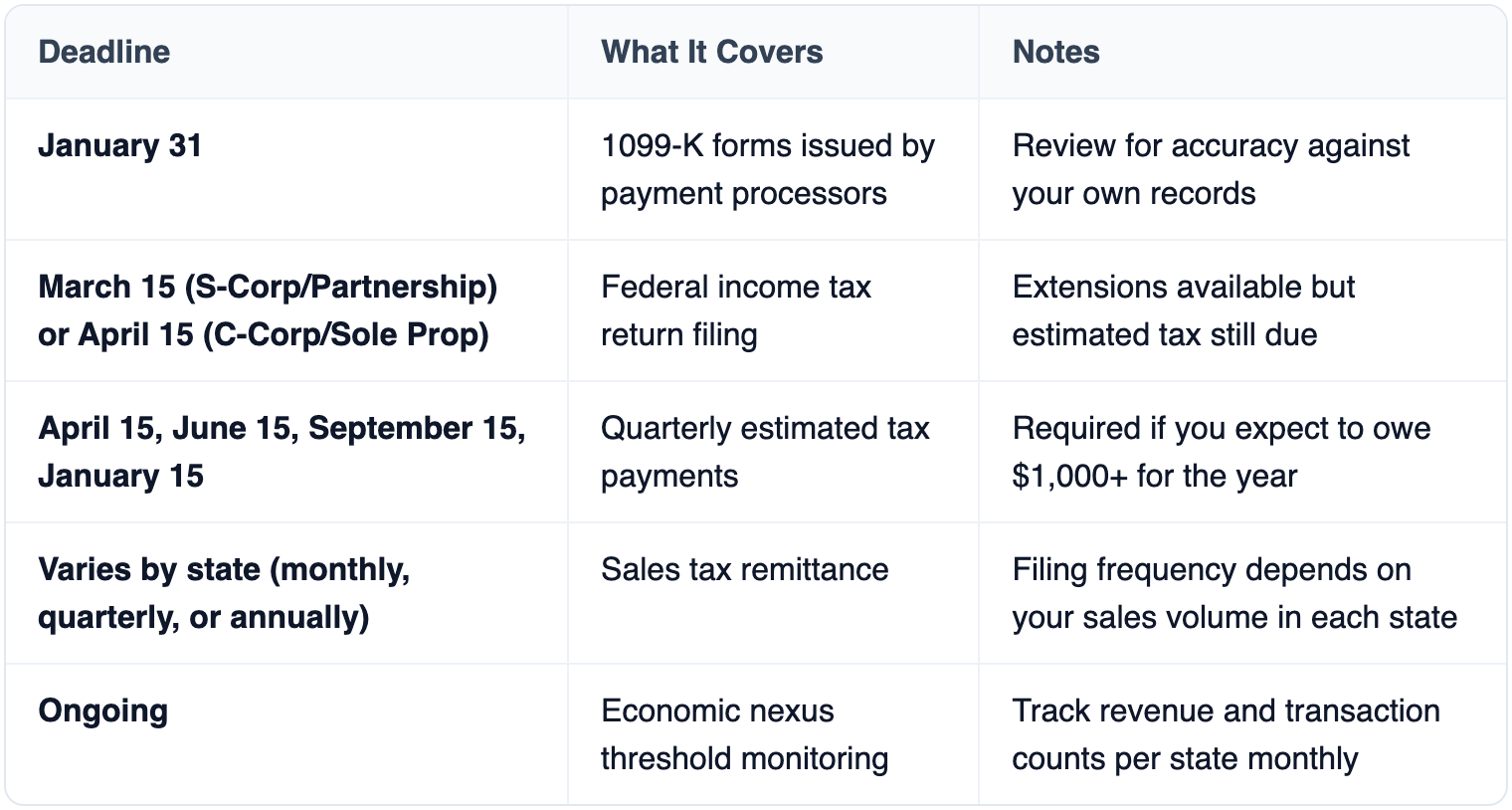

Finally, there's the sales tax puzzle. Since the 2018 South Dakota v. Wayfair decision, economic nexus rules mean your clients likely owe sales tax in dozens of states. Tracking thresholds, filing frequencies, and rate changes across jurisdictions is a significant workload that traditional accounting workflows weren't built for.

A standard chart of accounts won't cut it for an online retail business. You need accounts that reflect how money actually moves through your operations. Most e-commerce startups should add separate expense accounts for payment processing fees (broken out by platform if possible), shipping and fulfillment costs, and marketplace commissions. On the revenue side, it's smart to create distinct income accounts for each sales channel rather than lumping everything into one "Sales" line. This gives you channel-level profitability reporting without extra work at month-end. Your COGS section also needs more granularity than a typical business: separate lines for product cost, inbound freight, customs duties, and warehouse handling fees help you spot margin erosion early.

Here are five accounts commonly added for e-commerce:

E-commerce startups face a uniquely tangled tax situation because they often trigger obligations in states where they have no physical presence. Economic nexus thresholds vary by state, and crossing them mid-year means you need to register, collect, and remit sales tax on a rolling basis. Missing a threshold doesn't just mean back taxes: it means penalties and interest that can stack up quickly for a cash-strapped startup.

Not all accounting platforms handle online retail well. Here's what to prioritize when choosing yours:

Do I need a separate business bank account for my e-commerce startup? Yes, absolutely. Mixing personal and business funds makes bookkeeping a nightmare and weakens your liability protection if you're structured as an LLC or corporation. Open a dedicated business checking account before your first sale.

Should I hire an accounting firm or handle books myself at the seed stage? At the seed stage, a hybrid approach works best. Use accounting software to automate daily transaction recording, then hire an accounting firm for monthly review, tax planning, and compliance. This keeps costs manageable while ensuring accuracy during the period investors will scrutinize most.

How do I handle sales tax if I sell in all 50 states? You likely don't owe sales tax in all 50 states right away. Track your revenue and transaction count per state against each state's economic nexus thresholds. Register and collect only where you've crossed the threshold. Sales tax automation tools can monitor this for you.

What accounting method should an e-commerce startup use: cash or accrual? Most e-commerce startups should use accrual accounting. It matches revenue to the period when goods are delivered, not when cash arrives. This gives you a more accurate picture of profitability, and it's required once your business exceeds $29 million in average annual gross receipts.

When should a Series A e-commerce company bring accounting in-house? A Series A company processing thousands of transactions daily should have at least one in-house bookkeeper or controller. The volume of reconciliation work, combined with investor reporting requirements, typically justifies a full-time hire. Your external accounting firm then shifts to an advisory and audit-prep role.

Getting e-commerce accounting right from day one saves you from painful (and expensive) corrections later. Start with a clean chart of accounts tailored to online retail. Pick software that talks to your sales channels natively. Monitor your sales tax nexus exposure every single month. And don't wait until your books are a mess to bring in professional help: even a quarterly review from a qualified accounting firm can catch issues before they compound.

The startups that scale successfully aren't just the ones with the best products. They're the ones that know their numbers cold. Build that financial foundation now, and you'll thank yourself when investors, acquirers, or the IRS come knocking.