Defense startups face a financial reality most tech companies never encounter. Government contracts, ITAR compliance, and cost accounting standards create a web of requirements that can sink an otherwise brilliant company. Whether you're building autonomous drones or developing cybersecurity tools for the DoD, your accounting system needs to be as battle-tested as your product. This guide to accounting for defense startups breaks down everything you need to know, from chart of accounts design to tax deadlines, so you can focus on building technology that matters. Getting your financial house in order isn't just good practice. It's often a prerequisite for winning your first contract.

Accounting for defense startups is the practice of managing finances under the strict regulatory and compliance requirements imposed by government defense contracts. It matters because a single misstep can disqualify you from future contracts, trigger audits, or result in penalties.

Here are the three most important things to know:

Get these three right, and you've built a foundation that supports growth. Get them wrong, and you're fighting fires instead of winning contracts.

Your clients in the defense space operate under a level of financial scrutiny that most industries never face. The federal government isn't just a customer. It's a regulator with audit authority over your books. That single fact changes everything about how you structure your accounting.

The first major distinction is contract-based cost tracking. Unlike a SaaS company that tracks revenue by subscription tier, defense startups must allocate every dollar to specific contracts. Direct labor, materials, subcontractor costs, and even overhead must be traced or allocated to individual projects. This isn't optional. FAR Part 31 defines which costs are allowable, and DCAA auditors will test your system's ability to segregate them.

The second distinction is the incurred cost submission. Defense contractors must file an annual incurred cost proposal detailing actual indirect rates versus provisional billing rates. This process requires granular data that most startups simply don't collect unless their accounting system was designed for it. Miss this requirement and you risk payment delays, rate disputes, or worse. These two factors alone mean defense startups can't rely on the same accounting playbook as their commercial counterparts.

A standard chart of accounts won't survive first contact with a DCAA auditor. Defense startups need accounts that reflect the unique cost structures required by government contracting. The biggest difference is the separation of direct and indirect costs at the account level, not just in reports. You'll need distinct accounts for each indirect rate pool: fringe benefits, overhead, and general and administrative expenses. Naming conventions matter too. Auditors expect clarity, so "6100 - Direct Labor" and "6200 - Indirect Labor (Overhead)" should be immediately distinguishable. You'll also need accounts specifically for unallowable costs, clearly labeled and segregated so they never accidentally end up on a government invoice.

Here are five accounts commonly added for defense contractors:

Each of these accounts should have sub-accounts or tagging capabilities tied to individual contract numbers. This structure makes DCAA audits far less painful and keeps your billing accurate.

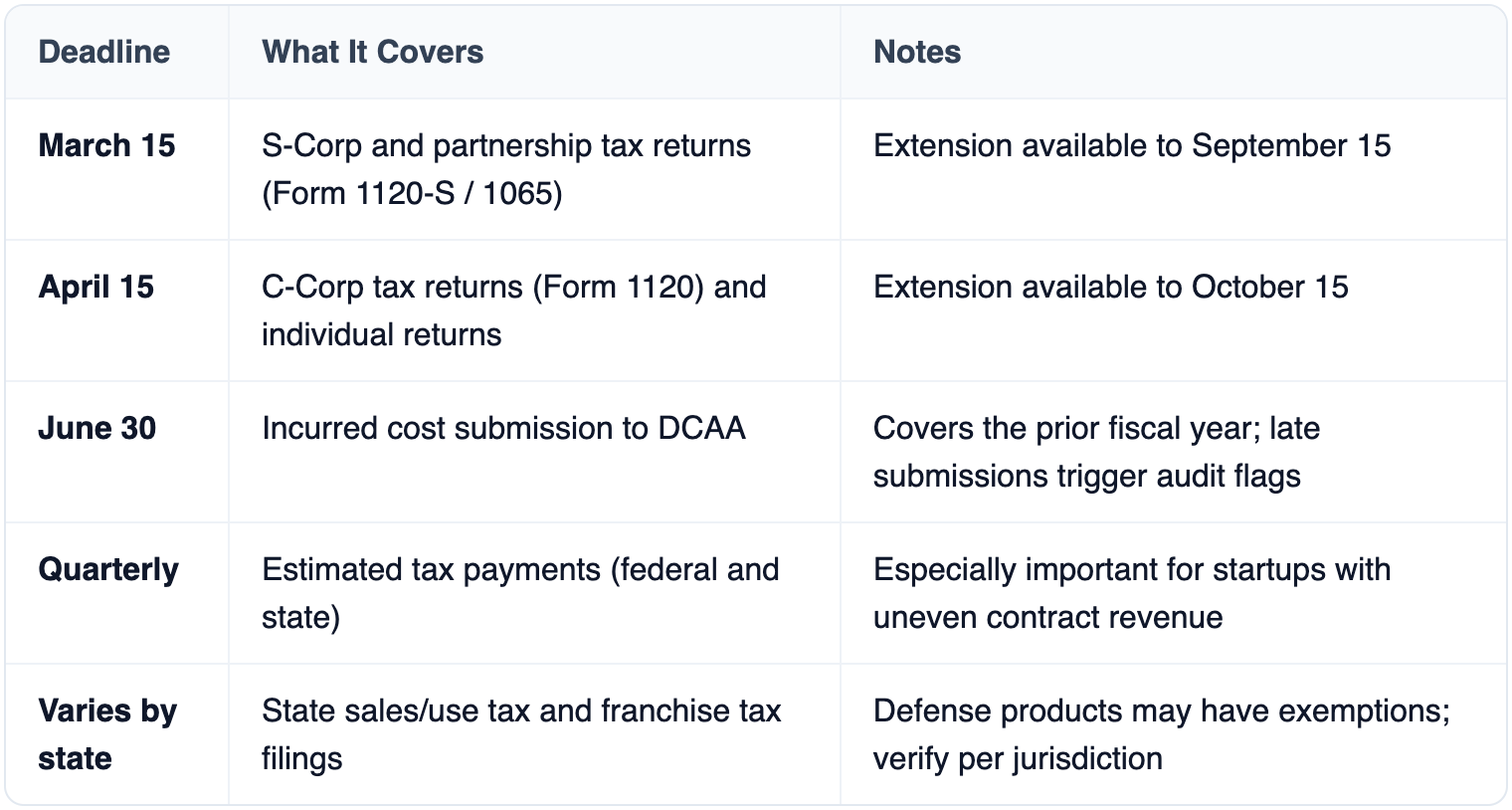

Defense startups face the same federal and state tax obligations as any business, but several deadlines carry extra weight because of government contract requirements. Your incurred cost submission deadline, for example, isn't technically a tax filing, yet missing it can freeze contract payments. R&D tax credits also deserve special attention since defense R&D spending often qualifies for substantial credits under IRC Section 41.

Don't treat the June 30 incurred cost deadline as an afterthought. It requires the same level of preparation as your annual tax return, and the consequences of a late or inaccurate submission can be severe.

The right accounting platform can mean the difference between passing a DCAA audit and scrambling to reconstruct records.

Do I need DCAA-compliant accounting from day one?

Yes. If you plan to pursue cost-type government contracts, your accounting system must meet DCAA standards before the pre-award audit. Retrofitting your books after the fact is expensive and time-consuming. Set up your system correctly at incorporation, even if your first contract is months away.

What's the difference between a cost-type and fixed-price contract for accounting purposes?

Cost-type contracts reimburse your allowable costs plus a fee, which means every expense is subject to audit. Fixed-price contracts pay a set amount regardless of your actual costs. Your accounting burden is heavier on cost-type contracts, but even fixed-price work requires compliant timekeeping and cost segregation if you hold any cost-type contracts simultaneously.

Should a seed-stage defense startup hire a specialized accounting firm?

Strongly consider it. A seed-stage company often can't afford a full-time controller with defense experience. A firm that specializes in government contractor accounting can set up your chart of accounts, establish compliant processes, and handle your first incurred cost submission. The cost is a fraction of what you'd spend fixing problems after a failed audit.

Can I use the R&D tax credit for defense-related development work?

In most cases, yes. Defense R&D spending on developing new products, improving existing technology, or creating prototypes typically qualifies under IRC Section 41. The credit can offset payroll taxes for startups with no income yet, making it especially valuable at the pre-revenue stage. Document your qualified research activities carefully.

How do I handle classified project costs in my accounting system?

Classified work requires careful compartmentalization. You can track costs by contract number without revealing classified details in your accounting records. Use generic project codes and maintain detailed records in a secure environment that meets your facility clearance requirements. Your accountant needs to know the cost structure without accessing classified technical information.

Getting accounting right isn't glamorous, but it's the backbone of every successful defense company. The startups that win repeat contracts and scale past Series A are the ones that built compliant systems early. They didn't wait for an audit notice to fix their timekeeping. They didn't scramble to create indirect rate pools the week before their incurred cost submission was due.

Start with a DCAA-compliant chart of accounts. Implement proper timekeeping on day one. Separate your allowable and unallowable costs clearly. And find an accounting partner who knows the defense space inside and out.

Your technology might be what wins the contract. But your accounting is what keeps it. If you're building a defense startup in 2026, treat your financial infrastructure with the same rigor you bring to your product. The companies that do this well don't just survive government audits. They turn clean books into a competitive advantage.