Cybersecurity is one of the fastest-growing verticals in tech, and the financial side of these companies is anything but straightforward. Between recurring revenue models, R&D tax credits, and compliance-heavy contracts, the accounting demands are unique. If you're a founder trying to keep your books clean or a firm serving this space, you need a specialized approach. This guide to accounting for cybersecurity startups covers the specific financial practices, tax considerations, and software criteria that matter most. Think of it as your go-to reference, whether you're pre-seed or scaling past Series B. Getting this right early saves you from painful corrections later.

Accounting for cybersecurity startups means tracking revenue, expenses, and compliance obligations that are specific to companies selling security products and services. It matters because investors, auditors, and acquirers all scrutinize how cybersecurity companies recognize revenue, capitalize development costs, and handle government contract accounting.

Here are the three most important things to know:

Even if you stop reading here, those three points will shape 80% of your accounting decisions.

From an accounting firm's perspective, your cybersecurity clients operate under constraints that most SaaS companies don't face. The first major difference is contract structure. Cybersecurity vendors frequently sell to government agencies and large enterprises under contracts with strict billing milestones, holdback provisions, and performance-based payment schedules. These aren't simple monthly subscriptions. You need to track deferred revenue with far more granularity than a typical B2B SaaS engagement requires.

The second distinction is the weight of compliance spending. Your clients in this space aren't just pursuing SOC 2 for marketing purposes. They're often contractually required to maintain certifications like FedRAMP, CMMC, or ISO 27001 as a condition of doing business. These costs are material, recurring, and need to be treated as cost of revenue or a dedicated compliance expense line, not lumped into overhead.

Third, cybersecurity startups often maintain significant deferred revenue balances because of annual or multi-year prepaid contracts. Mishandling these balances distorts your client's financial picture and creates real problems during due diligence. A senior accountant working with this vertical needs to understand the revenue timing implications of every contract type the company signs.

A standard SaaS chart of accounts won't fully serve a cybersecurity company. You'll need accounts that reflect the unique cost structure of building and selling security products. Threat intelligence feeds, penetration testing tools, and cloud infrastructure for security operations centers (SOCs) all deserve their own expense accounts rather than being grouped under generic categories like "software" or "hosting." On the revenue side, you'll want separate accounts for product subscriptions, professional services (incident response, consulting), and managed security services. This separation is critical for calculating gross margins by business line, which investors and board members will ask about. Naming conventions should be specific enough that anyone reviewing the general ledger can identify the business purpose without cross-referencing contracts.

Here are five accounts commonly added for this vertical:

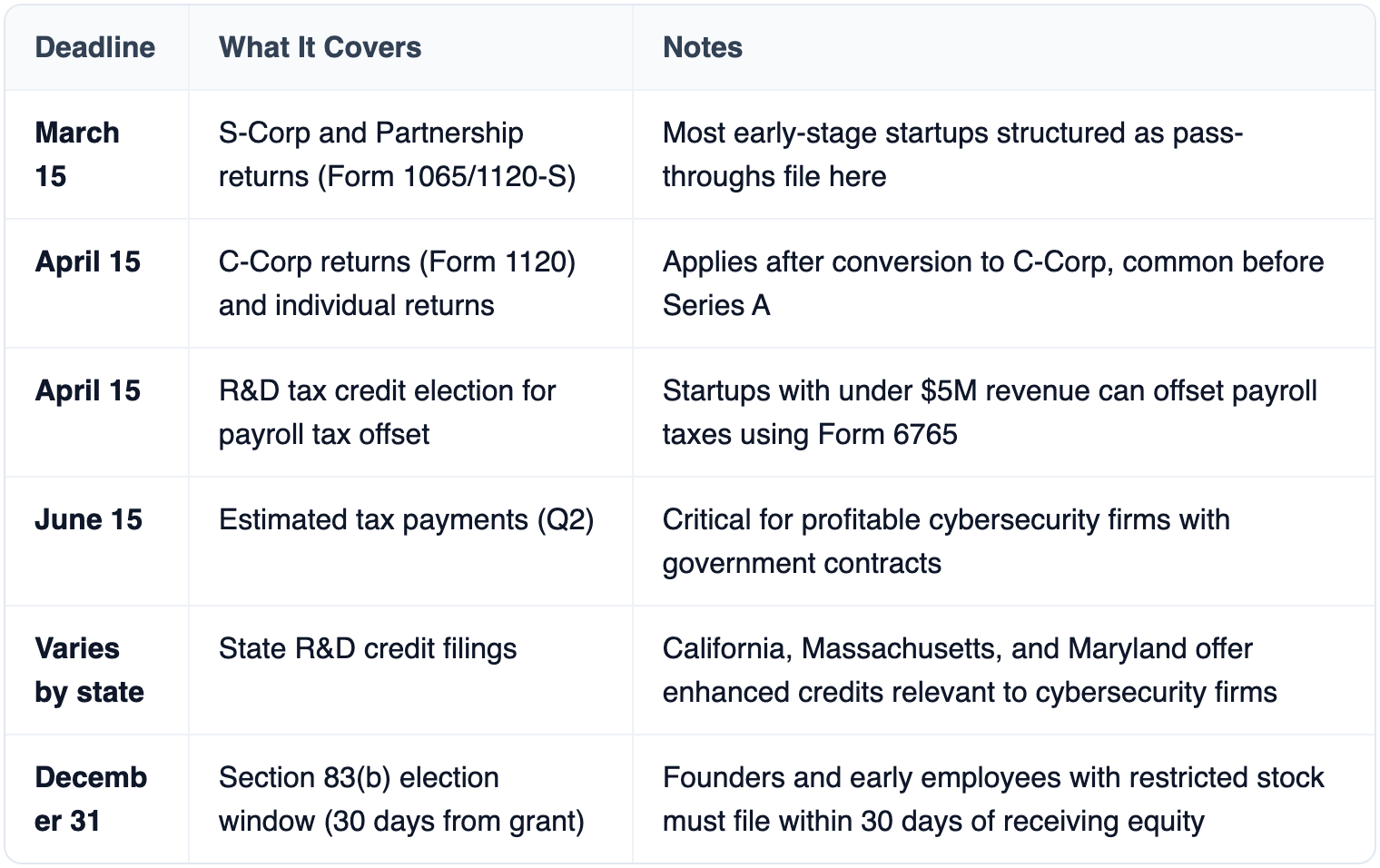

Cybersecurity startups face a tax environment shaped by heavy R&D spending, potential government contracts, and multi-state or international sales. The R&D tax credit under IRC Section 41 is often the single largest tax benefit available, but the 2022 amortization requirement under Section 174 means you can no longer deduct R&D expenses immediately. You must plan for this from your first fiscal year.

Keep a rolling calendar. Missing the payroll tax offset election alone can cost an early-stage cybersecurity company $250,000 or more per year.

Choosing the right accounting platform depends on your company's specific operational needs. Here's what to prioritize:

Do cybersecurity startups need a specialized accountant or CPA firm?

Yes. A generalist accountant will likely mishandle R&D cost capitalization, multi-element revenue arrangements, and government contract accounting. Look for firms with experience in SaaS, government contracting, or both. The cost difference between a specialist and a generalist is small compared to the cost of restating financials before a funding round.

How should a seed-stage cybersecurity startup handle its books?

At the seed stage, keep it simple but structured. Set up your chart of accounts with cybersecurity-specific categories from day one. Track R&D hours and expenses meticulously, even if you're not yet filing for the tax credit. Use cloud-based accounting software and reconcile monthly. Don't wait until Series A due diligence to clean up your books.

What's the biggest accounting mistake cybersecurity startups make?

Failing to separate revenue streams. Lumping subscription revenue, professional services, and managed security services into a single line makes it impossible to calculate accurate gross margins by segment. Investors will flag this immediately, and fixing it retroactively across multiple periods is painful.

Can cybersecurity startups claim the R&D tax credit?

Absolutely. Most cybersecurity product development qualifies under the four-part test: technological uncertainty, process of experimentation, technological in nature, and qualified purpose. Startups with less than $5 million in gross receipts can apply the credit against payroll taxes, which is valuable before you're profitable.

How does FedRAMP certification affect accounting?

FedRAMP costs are substantial, often $500,000 to $1.5 million for initial authorization. These should be capitalized as an intangible asset if they provide future economic benefit over multiple periods, then amortized over the expected useful life of the authorization. Annual maintenance costs are expensed as incurred.

Getting your accounting right from the start isn't just about compliance. It's about building a financial foundation that supports fundraising, government contracts, and eventual exit. Cybersecurity startups that treat accounting as an afterthought consistently face delays during due diligence, miss valuable tax credits, and struggle to demonstrate unit economics to investors.

Start with a proper chart of accounts. Set up revenue recognition policies that match your contract structures. Track R&D costs with enough detail to support tax credit claims. And find an accounting firm that actually understands the cybersecurity vertical.

The companies that get acquired or go public aren't just the ones with the best products. They're the ones whose books tell a clear, accurate financial story. Make sure yours does too.